Tech Earnings Recap: Post-DeepSeek Chaos

A deep dive into this week’s tech earnings, covering ASML, Meta, Microsoft, and more!

DeepSeek R1 and R1-Zero, side projects from a Chinese hedge fund, triggered a massive sell-off this week across the supply chain from TSMC to NVIDIA and Broadcom. NVIDIA took the biggest hit, losing $583 billion in market value, the largest single-day decline in history! I have a lot to cover in this article but before doing so I’d like to briefly touch on why DeepSeek’s new models are important and what it means for the industry.

DeepSeek

DeepSeek models use a technique called distillation, where a larger, more advanced AI model trains a smaller one to perform at a similar level with fewer resources. Instead of learning from scratch, the smaller model picks up reasoning patterns and decision-making skills from the larger model, making it far more efficient. In other words, the larger model is teaching the smaller one how to think and behave. DeepSeek has also developed R1-Zero, which takes this a step further by figuring out reasoning skills on its own, without human-labeled data. By using these methods, DeepSeek is able to create powerful AI models at a fraction of the cost of competitors like OpenAI while keeping performance strong

While not cutting-edge, its efficiency is a breakthrough. AI has been expensive, limiting adoption, but a cheaper yet similarly powerful model makes it more accessible for businesses to experiment without heavy investment. This aligns with Jevons Paradox, where efficiency drives greater demand, benefiting companies like Meta, which thrives on AI-driven engagement. More on Meta later on.

Earnings This Week

I will try my best to keep things concise, touching on the key points. Let’s begin with the cog that allows the rest of the industry to function.

ASML

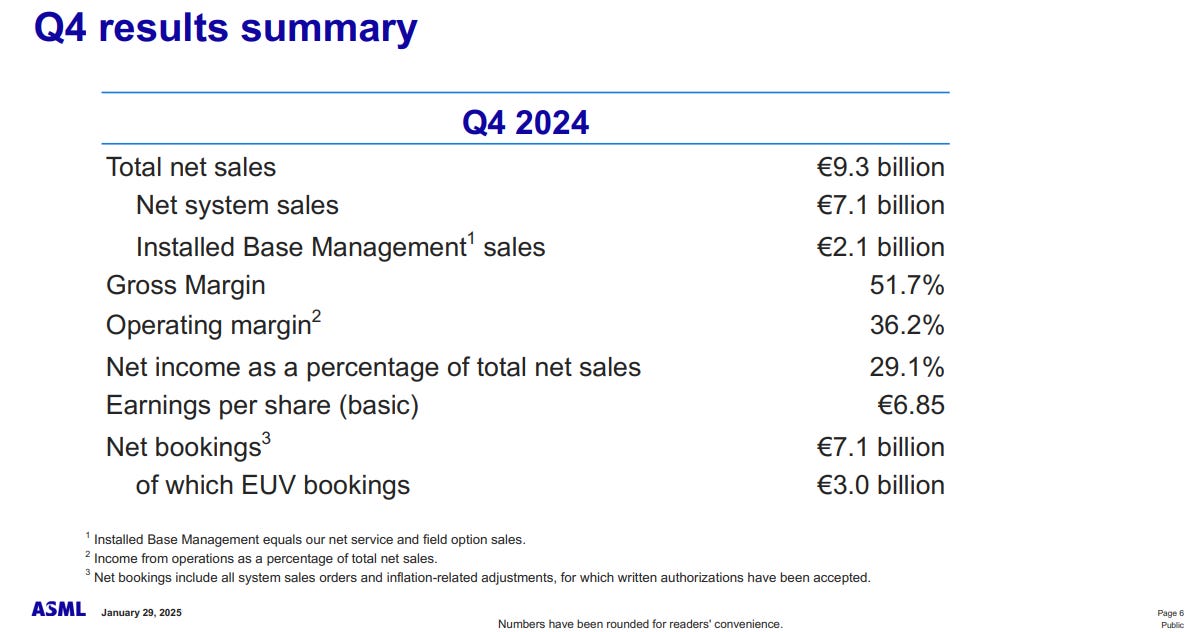

2024 was going well for ASML until its Q2 earnings in July revealed a 15% YoY year revenue decline and raised concerns about stricter U.S. export restrictions to China. The situation worsened after its Q3 results in October, where an accidental early release of earnings exposed a reduced 2025 revenue forecast and a sharp drop in orders, sending the stock tumbling by ~16%. The mood was brighter Wednesday morning after Q4 earnings, despite ASML plunging by ~10% earlier on in the week due to the DeepSeek sell-off. ASML opened 11% higher post-earnings reflecting the optimistic tone of investors. What’s there to be optimistic about, DeepSeek just ended the AI trade? I hope that this isn’t your immediate thought. Let’s see where the optimism stems from.

The first figure I’ll start with is net bookings which came in at €7.1bn for Q4, completely surpassing analysts’ estimates of €4bn. Of that, €3 billion came from EUV machines, showing that chipmakers are still aggressively expanding capacity.

TSMC, one of ASML’s biggest customers, announced $38 to $42 billion in capex for 2025, with approximately 70% going toward advanced process technologies. TSMC is also ramping up its US presence with two fabs under construction in Arizona to diversify supply chains. This ties into the next key shift as the US overtook China as ASML’s top sales destination for the first time this year, a direct result of tightening export restrictions.

Looking at 2024 as a whole, ASML reported €28.3 billion in total net sales and €7.6 billion in net income, coming in roughly flat compared to the previous year. While growth in absolute numbers was limited, ASML isn't a stock driven by short-term revenue spikes but by its role as the backbone of cutting-edge semiconductor manufacturing. The company faced a softer demand environment with weaker memory spending and geopolitical restrictions impacting China sales, yet it maintained strong profitability with a 51% gross margin. With high-NA EUV (the next generation of extreme ultraviolet lithography enabling smaller and more powerful chips) adoption on the horizon and a solid order book, the focus now shifts to how quickly chipmakers ramp up spending in 2025.

2025 guidance came in strong with ASML projecting net sales between €30 billion and €35 billion and gross margins in the 52 to 53% range. Management expects a pickup in demand as AI-driven chip production ramps up, with key customers like TSMC, Intel, and Samsung increasing investments in advanced nodes (smaller, more efficient transistor architectures for AI and high-performance computing). High-NA EUV remains a major growth driver, and with a record backlog, ASML is well-positioned for recovery as chipmakers push forward with next-gen fabs.

ASML remains a critical pillar of the semiconductor supply chain, with its performance closely tied to the growing demand for computing power. As companies invest heavily into AI infrastructure, ASML’s equipment is essential for producing the advanced chips that power this shift, making it, in my view, a must-have in any tech portfolio. However, any signs of weakening demand will not sit well with investors, and as we’ve seen over the past year, ASML’s stock prices are prone to sharp daily swings.

Meta

Meta operates across two key segments: Family of Apps (FoA), which drives the bulk of its revenue through advertising, and Reality Labs, focused on hardware and next-generation technologies. 2024 was defined by Meta's aggressive push into AI, with advancements in generative AI tools and automation enhancing ad targeting and content recommendation systems.

Meta was the only hyperscaler that didn’t drop on the Monday after DeepSeek R1 was announced because its AI strategy is built around open-source adoption rather than reliance on closed models. Unlike OpenAI and Anthropic, Meta isn’t reliant on monetising proprietary models, meaning efficiency breakthroughs like DeepSeek’s only accelerate AI adoption, which benefits its ecosystem.

Q4 performance reflected strong revenue growth and record profitability, fueled by AI-driven ad optimization and higher engagement across its platforms. Quarterly revenue hit $48.39 billion, up 21% YoY, with net income surging 49% to $20.84 billion. The Family of Apps segment, which includes Facebook, Instagram, and WhatsApp, remained the core revenue driver, generating $46.8 billion in ad revenue, while Reality Labs posted a $4.97 billion loss, reflecting ongoing investment in emerging technologies, including AR, VR, and next-generation hardware.

Overall, Meta closed out 2024 with strong revenue growth and record profitability, driven by AI-powered ad targeting and increased engagement across its platforms. Full-year revenue hit $164.5 billion, up 22% YoY, while net income surged 59% to $62.4 billion. Not bad, but the key question remains. Will this spending translate into real revenue growth? Meta’s Q4 numbers didn’t disappoint, with strong ad growth and record profitability, but the spending story remains the biggest debate throughout the rest of 2025.

Meta expects revenue growth to continue in 2025, with Q1 guidance set between $39.5 billion and $41.8 billion, reflecting an 8 to 15% YoY increase. Expenses are projected between $114 billion and $119 billion for the year, with the biggest driver being infrastructure costs as Meta scales its AI capabilities. The high CapEx commitment underscores its long-term AI ambitions, but the real test will be whether this investment leads to meaningful revenue growth. AI-driven ad efficiency has clearly paid off, with a 14% increase in average ad prices, but sustaining that momentum as costs rise will be crucial. Reality Labs remains a heavy drag on profitability and the company has yet to demonstrate a clear path to monetization.

I like Meta’s positioning for 2025, but there are significant questions that need answering. I believe they have the vision and ability to execute, but it won’t be a smooth ride. The race to develop a reasoning model with mid-level developer capabilities will be tight, and the winner will gain a significant edge that could drive stronger revenue.

Now, moving on to one of their biggest competitors in the AI space.

Microsoft

I’ve saved the earnings release with the weakest market reaction for last. Microsoft operates across three main segments: Productivity and Business Processes, Intelligent Cloud, and More Personal Computing. 2024 was the year of solidifying its AI leadership, integrating Copilot across Office 365 and rolling out AI-powered features across its ecosystem.

A quick note, Microsoft follows a fiscal year ending in June, making this its Q2 FY25 earnings for the quarter ending December 31.

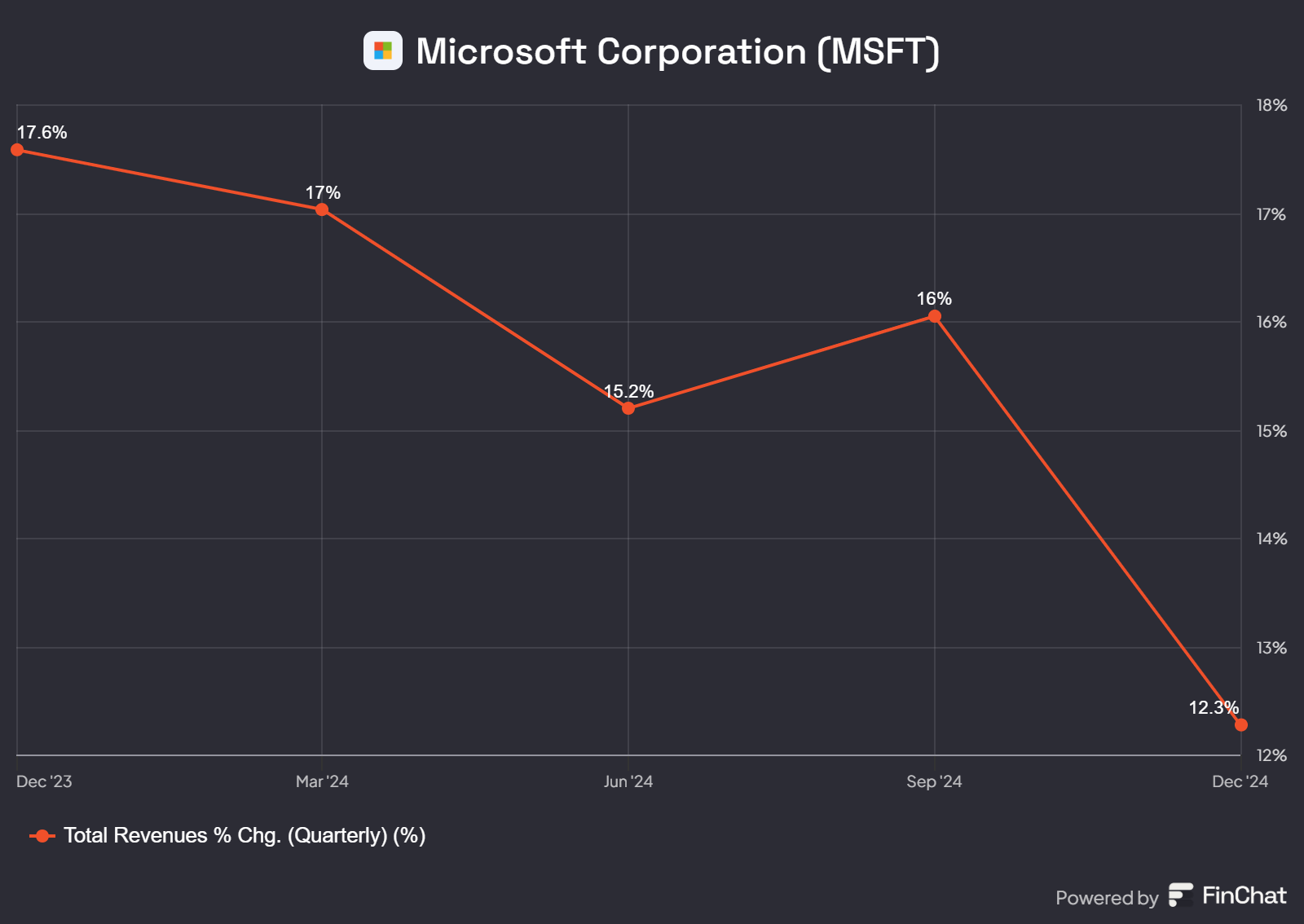

Microsoft closed out the quarter with $69.6 billion in revenue, up 12% YoY, and $24.1 billion in net income, up 10% YoY. Azure and other cloud services grew 31% YoY, fueled by enterprise demand for AI workloads, while Microsoft Cloud hit $40.9 billion in revenue, up 21% YoY. Mr Nadella confirmed that Microsoft’s AI business has now surpassed a $13 billion annual run rate, up 175% YoY, meaning that if current AI revenue levels hold, Microsoft would generate $13 billion from AI over the next 12 months.

AI was also key in Microsoft 365 growth, with Copilot adoption driving higher-priced E5 subscriptions, while LinkedIn benefited from AI-driven engagement tools. More Personal Computing remained flat, but with AI-powered PCs on the horizon, Microsoft sees room for future growth in this segment.

Investors were disappointed because while Microsoft's revenue and earnings beat expectations, the deceleration in revenue growth alongside surging capital expenditures raised concerns about profitability. Revenue growth is slowing just as Microsoft is ramping up $80 billion in AI infrastructure spending. While AI is driving incremental gains, it is not accelerating overall revenue growth enough to justify the rising costs. This dynamic has put pressure on margins and raised doubts about whether AI investments will translate into profitable, long-term growth.

What Microsoft is doing is solid but I feel that its sheer size and complexity, in terms of business segments, make sustained outperformance challenging. With revenue growth slowing and CapEx rising, the risk-reward balance looks unfavourable. There seems to be limited upside but significant downside if execution falters, and there are more compelling opportunities elsewhere. The MSFT chart doesn’t excite me either as it’s been ranging for a while whilst its competitors (META, GOOGL) have seen strong upside.

Notable Mentions

Apple

Apple reported Q1 FY25 revenue of $124.3 billion, up 4% YoY, just above expectations, with EPS of $2.40, a 10% increase. Services grew 14% to a record $26.3 billion, while iPhone sales fell 1%, weighed down by an 11% drop in China, where Apple Intelligence has yet to roll out. In markets where it launched, the feature drove stronger iPhone 16 sales, boosting upgrades. Investors reacted relatively positively, with shares rising 3% after-hours, but nothing to catch the headlines. While the numbers were solid, this was more of a steady quarter rather than a standout one. Apple isn’t a name that excites me. It remains behind in AI, and this quarter did little to change that.

Atlassian

Unlike Apple, Atlassian is a name that excites me, and they delivered a strong earnings beat. Revenue grew 21% YoY, driven by a 30% increase in cloud revenue, reflecting a successful transition to a subscription-based model. Shares surged 20% higher after-hours reflecting how investors felt about the beat. As AI adoption expands and becomes more cost-efficient, software companies like Atlassian could be among the biggest beneficiaries as their offerings become more tailored and intelligent.

IBM

Perhaps a name that has gone under the radar, IBM has plenty to offer in the AI space. They delivered a solid earnings beat with EPS of $3.92, surpassing estimates of $3.79 on $17.55 billion in revenue. The standout was their generative AI business, which grew by $2 billion from the previous quarter, now exceeding $5 billion in total revenue. This sent the stock up 8% after hours, reflecting the market’s confidence in IBM’s growing AI presence.

Upcoming Earnings

Next up: earnings from Google, Rambus, AMD, Qualcomm, ARM, and Amazon, making for another busy week.

I hope that you enjoyed the earnings recap, please feel free to reach out if you have any questions!

Disclaimer: This article is for informational purposes only and should not be considered financial or investment advice. The views expressed are my own and based on publicly available information, market trends, and personal analysis. I have positions in Meta and ASML, but these may change at any time. Readers should conduct their own research and consult a financial professional before making any investment decisions.