Rigetti Computing: Deep Tech, Shallow Revenue

This article is a deep dive on Rigetti Computing Inc, a player in the quantum computing space which has seen a lot of hype. Is the hype justified?

Today, I’ll be doing a deep dive on one of the faces of the quantum computing space, Rigetti Computing. If you haven’t already, check out my article where I explain what quantum computing is and how it works. A quick detour will make this article easier to read, I promise!

History

Rigetti Computing was founded in 2013 by Chad Rigetti, a physicist who previously worked on superconducting qubits at IBM. The goal from the beginning was to build a commercially viable quantum computer by controlling every layer of the stack, from chip fabrication through to cloud-based software access. In 2017, Quantum Cloud Services was launched, offering users remote access to Rigetti’s quantum processors. In 2018, Fab-1 opened in Fremont, California, becoming the first dedicated quantum chip fabrication facility operated by a start-up. This allowed Rigetti to iterate on hardware designs without relying on external foundries. Over the following years, Rigetti developed several generations of superconducting quantum processors, including the Aspen-series, with steady improvements in coherence times, gate fidelity and architecture. Systems were integrated into Amazon Braket and Microsoft Azure, expanding availability to enterprise and research users. Partnerships were formed with agencies including DARPA, the US Air Force and Innovate UK. In March 2022, Rigetti went public through a SPAC (Special Purpose Acquisition Company) merger with Supernova Partners Acquisition Company II, in a transaction that valued the business at approximately $1.5bn. Quite lofty, I must say, considering that they haven’t produced any profits, but more on that later. After listing, execution challenges and delays in processor development led to weaker financial performance and a sharp decline in share price. A strategic reset followed in 2023. Subodh Kulkarni was appointed chief executive and initiated a revised operating plan focused on performance improvements, cost control and streamlining product development. Later that year, Rigetti launched Ankaa-1, an 84-qubit processor based on a square lattice architecture. The design achieved a two-qubit fidelity of 98.2% and served as the basis for internal testing of larger-scale systems.

Products

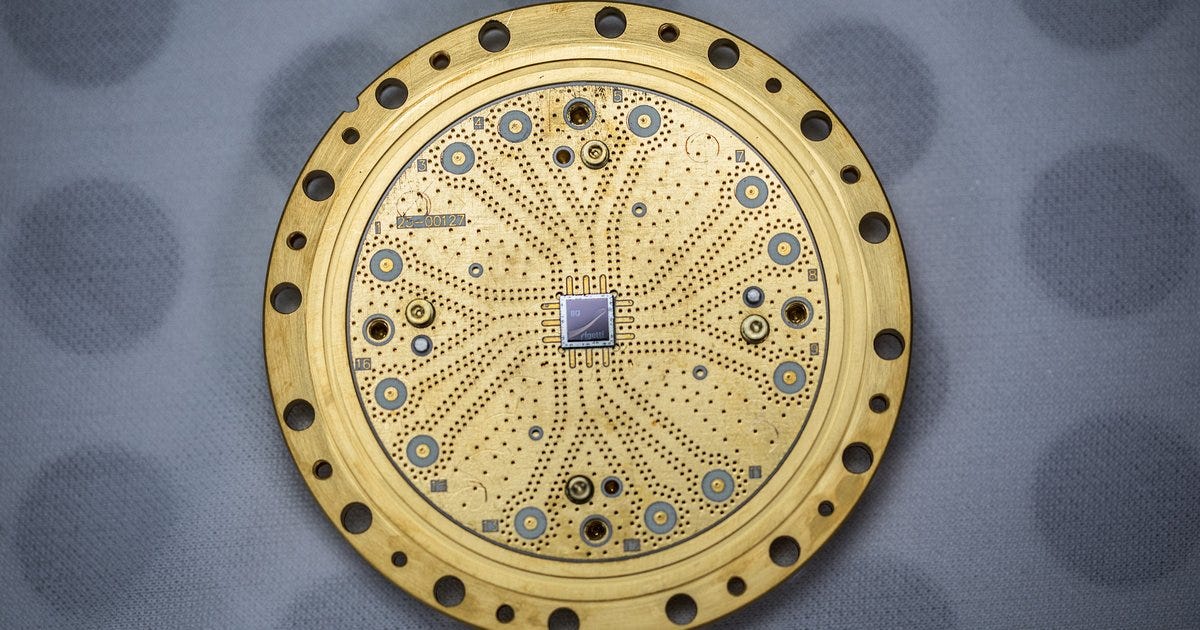

I’ve mentioned a few of the products already but let’s start with Ankaa-3. This is the most advanced quantum processor Rigetti has built to date and is the system currently active on Quantum Cloud Services. It contains 84 superconducting qubits arranged in a square lattice, a layout that improves connectivity between qubits and allows for more complex circuits to be executed with fewer errors. Each qubit is connected to several neighbours, enabling multi-qubit operations to run in parallel without requiring long routing sequences, which would otherwise increase noise and failure rates.

Gate operations are triggered by microwave pulses, and performance is largely defined by two metrics: fidelity and crosstalk. Fidelity measures how accurately a gate performs the intended quantum operation. Crosstalk refers to unintended interference between qubits, where a control signal meant for one qubit partially affects another. This degrades performance and limits how many gates can be run in sequence. Ankaa-3 introduces improvements in both areas. Rigetti has reduced crosstalk through better control pulse shaping and calibration techniques, allowing more reliable gate execution across the full chip. The system is accessed through Quantum Cloud Services, which serves as Rigetti’s full-stack delivery platform. This is where users write, compile and run quantum programs on live hardware. It supports Quil, Rigetti’s native programming language, as well as integration with standard frameworks like Qiskit and Cirq. Most workloads are hybrid, meaning part of the problem runs on classical hardware and the quantum processor is used to accelerate the part that benefits from quantum parallelism. The entire workflow, from job submission through to result retrieval, is handled within the platform, either via direct API or through managed cloud environments like Amazon Braket and Microsoft Azure.

Ankaa-3 is used by external clients for research, optimisation problems and algorithm benchmarking, and also supports internal testing for calibration protocols and hardware scaling. It’s the third release under the Ankaa architecture and represents Rigetti’s most stable and highest-performing system currently in operation.

Separate from its cloud-delivered systems, Rigetti has developed the Novera QPU, a standalone quantum processor offered as a physical hardware product. Novera uses the same core superconducting technology as Ankaa, with 84 qubits arranged in a square lattice, but it’s not part of an integrated system. It doesn’t include the cryogenic infrastructure, control electronics or software interface used in Ankaa. Instead, Novera is delivered as a packaged quantum chip, designed for external integration by clients who have their own cryogenic and control environments. The main distinction is that Ankaa is accessed remotely as a service, with Rigetti operating the full stack and managing the entire runtime. Novera, by contrast, is intended for deployment into a client’s own facility, where it can be paired with independent infrastructure. This opens the door for use cases where cloud access is not permitted or where direct physical control is required, such as classified research or sovereign system development. It also shifts responsibility for system performance and maintenance away from Rigetti and onto the client. Novera is available for purchase through a request-based model. Clients must submit a form and go through a qualification process, which effectively limits sales to organisations with specific technical requirements and infrastructure. While it will not generate the same volume of usage-based revenue as Ankaa, it reflects a different go-to-market strategy, enabling Rigetti hardware to be used in environments where cloud access is either impractical or restricted. It also marks the first time Rigetti has positioned itself as a direct hardware supplier, rather than purely a service provider.

Alongside its hardware, Rigetti also develops a proprietary software stack designed to interface directly with its quantum systems. At the core is Quil, Rigetti’s low-level instruction language, and pyQuil, a Python-based toolkit that allows users to write, compile and simulate quantum circuits. These tools are tightly integrated with the hardware, enabling access to native gate definitions, pulse-level controls and system-specific calibration routines. This gives researchers greater flexibility when designing hardware-aware algorithms and allows for more efficient use of quantum resources. It also serves a strategic purpose. The more users that build infrastructure around Rigetti’s tools, the harder it becomes to switch to a different stack. It reminds me of how NVIDIA locked in developers through CUDA. What began as a programming framework ended up becoming one of the most effective moats in the entire computing industry. Developers built infrastructure around it, optimised their workflows for it, and eventually became reliant on it. Switching was no longer just a technical decision, it became an operational headache. Of course, I am not comparing CUDA to pyQuil at all, however, it’s clear that Rigetti appears to be moving in the same direction. By controlling the full stack and promoting its own language and SDK, it’s not just offering a way to run quantum circuits. It’s building an environment that makes it harder to leave. If researchers and institutions standardise their tooling around Rigetti’s software and hardware, the switching costs rise sharply. That kind of lock-in is rare at this stage of the market and could prove more valuable than any one hardware milestone.

Financials

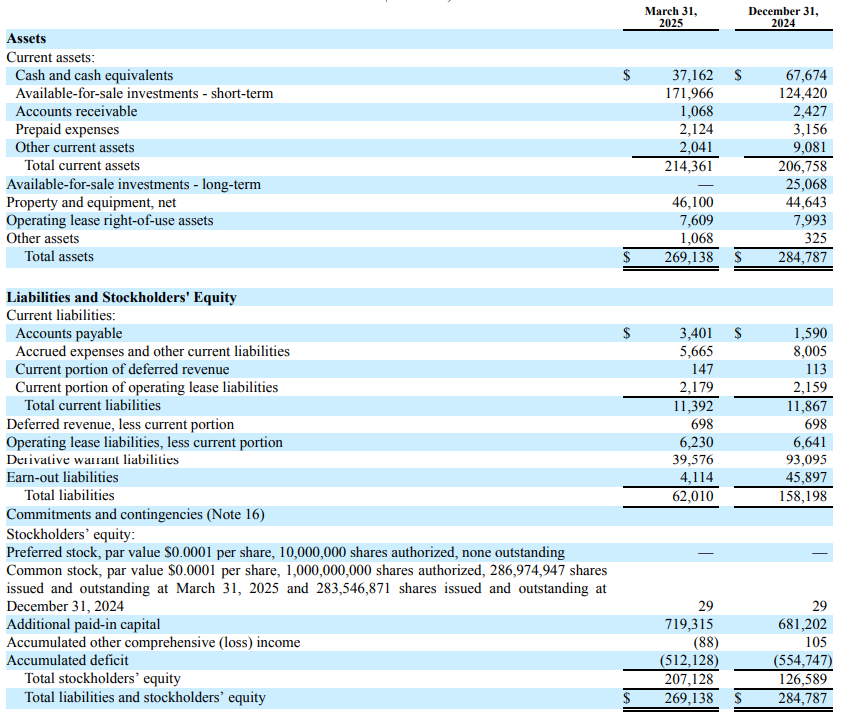

As pretty much every quantum computing company, Rigetti have yet to turn a profit. And although Quantum Computing Inc reported positive income for Q1, I’m not accepting that as profit as it stemmed from accounting wizardry relating to warrants. Rigetti’s financial performance reflects a business still operating in deep R&D mode, with minimal revenue leverage, a structurally high cost base and a funding model built on external capital rather than operating cash flow. Over the last twelve months, Rigetti generated $9.2mn in total revenue, down from $10.8mn the year prior and well below the $13.1mn peak reported in 2022. Despite the variability, these are not product-driven revenue streams. Most of the income continues to come from government contracts, including public sector grants and research collaborations tied to specific development milestones. There is little in the way of recurring revenue from commercial clients, and Rigetti’s core offerings have yet to scale in any meaningful way. Losses, by contrast, are not only persistent but accelerating. Net loss for the last twelve months was $137.6mn. The year before, it was $201mn. Cumulatively, Rigetti has posted over $450mn in losses since 2021. The sharp step-up in 2024 was driven by several non-cash charges, including fair value adjustments and stock-based compensation, but even on a pure cash basis, the core business is burning through capital. Gross margin remains negative. There is no evidence of operating leverage, and no marginal improvement in unit economics tied to revenue growth.

Looking at the cost base, research and development remains the dominant expense. In Q1 2025, Rigetti spent $15.5mn on R&D, accounting for 70% of total operating expenses. General and administrative costs came in at $6.6mn, or 30%, with no material change from the year before. The structure reflects the nature of the business: highly technical, fabrication-intensive, and run entirely in-house. It also means Rigetti has no real lever to pull when top-line performance stalls. The cost base is embedded. Even with cost controls in motion, the platform remains expensive to operate. Operating cash flow for the quarter was negative $13.7mn, an improvement from negative $19.1mn in Q1 2024, but not enough to shift the narrative. That figure includes salaries, chip development, cryogenic infrastructure and platform maintenance. Capital expenditure was low at $2.5mn, consistent with Rigetti’s asset-light model following the build-out of Fab-1. Most of the spending flows through the income statement, which means losses translate almost directly into cash burn. You can tweak headcount or freeze marketing, but when your platform is built around running quantum systems at 10 millikelvin, you are not exactly lean by design.

To stay solvent, Rigetti raised $75mn in 2023 through equity issuance. As of year-end, it held $105mn in cash and equivalents. At the time, that looked like roughly a year of runway. In reality, cash dropped to $64.3mn by the end of Q1 2025, implying a quarterly burn of over $40mn. Even if cost cuts are now in motion, the adjusted runway is closer to six months. A cost reduction plan was announced in early 2024, targeting a 30% cut in quarterly spend, but the Q1 numbers suggest it hasn’t flowed through yet. The SPAC proceeds from 2022, which totalled more than $260mn, are now largely gone.

Put plainly, Rigetti isn’t in a comfortable position, but is far from distressed. Cash and short-term investments total over $200mn, and there is no debt to service. Most of the liabilities are non-cash, and current obligations are minor. The real issue is not liquidity. It’s productivity. Unless revenue begins to scale, that cash will eventually get spent on salaries, hardware maintenance and platform support. But for now, the balance sheet gives them time to figure it out.

So why is Rigetti valued so highly? On paper, the valuation makes little sense. Despite what I’ve just mentioned about losses etc, the market is valuing it at over $3bn. The disconnect between financial performance and market capitalisation is not subtle. So what is driving it?

The first explanation is option value. Quantum computing is seen as a long-horizon technology bet, where the potential payoff dwarfs the initial capital at risk. If it works, it could reshape entire industries. If it fails, the downside is capped, with investors losing a couple of hundred million. Rigetti’s valuation reflects that optionality. Investors are not paying for near-term revenue. They are paying for a shot at future dominance. The second factor is scarcity. There are very few listed quantum computing companies, and even fewer with end-to-end control over hardware, fabrication and platform delivery. Rigetti builds its own superconducting chips, operates its own quantum cloud, and has deployed multiple generations of live systems. If you want public market exposure to physical quantum infrastructure, there are not many choices. The third is momentum. Rigetti trades at a low nominal share price, which draws retail attention. It has a clean narrative, a high-profile sector, and regularly appears in thematic flows. That positioning creates bursts of volume and price action that have little to do with fundamentals. Trading activity often reflects sentiment more than cash flow. And finally, there is a strategic angle. Quantum hardware is increasingly treated as critical infrastructure, both in national security and advanced computing. Governments are funding domestic programmes, and large corporates are positioning around quantum IP. Even if Rigetti never becomes profitable, it may still matter. That perceived strategic relevance supports a valuation that exceeds the underlying numbers. In short, the valuation is not anchored to what Rigetti is today. It’s a premium on what it could become. And for now, the market is still willing to pay for that possibility.

Competitors

Rigetti operates in a small group of quantum hardware firms. The most direct public peer is IonQ, which builds its systems using trapped-ion technology rather than superconducting qubits. IonQ has reported higher revenue and stronger gross margins, and trades at a premium. The two companies are not competing on architecture, but they are competing on narrative: control over the hardware, ownership of the stack, and long-term platform potential. Among private firms, PsiQuantum is building a photonic system and has raised over $600mn in venture funding. Quantinuum, formed by Honeywell and Cambridge Quantum, is backed by a large industrial parent and runs a tightly integrated hardware and software model. Neither is public, but both are well funded and active. Big tech is also in the picture. IBM, Google and Amazon have in-house quantum teams, and in some cases already offer access through cloud services. They have more capital and deeper enterprise reach, but less flexibility. Rigetti’s positioning rests on speed, iteration and full-stack control. Whether that is enough to compete long term remains an open question. The landscape is thin, but it’s crowded. Rigetti is one of the only ways for public investors to get direct exposure to quantum hardware, but the space is moving quickly and expectations are rising.

Trading Opportunities

I’m personally torn on whether Rigetti is a good investment. Which automatically means it isn’t a good investment if I’m unsure. I would treat Rigetti as more of a trade than an investment and by that, I mean trading it both ways. Understandably, Rigetti is heavily shorted. This means that a significant portion of the floating shares have been shorted by investors expecting the price to fall. Looking at data from Nasdaq below, at the end of April there were 66mn shares sold short, with a days-to-cover ratio of 3.2.

This means that if the stock were to rise sharply, it would have taken over three full trading days of average volume for short sellers to close their positions. I feel like being short at low-ish levels is a recipe for disaster, as given the current market sentiment, I’d assign a higher probability of a momentum burst leading to a short squeeze as opposed to the price grinding lower. However, having said that, Rigetti has been pushing higher. With $12 being nearly broken, I can see Rigetti reaching ~$16 within the next few weeks which at that point would, in my opinion, be a relatively okay level to be short. Of course, that depends on the market sentiment. But by using an options strategy, one could profit either way. In theory, an ideal trade would be a bull call spread followed by a long put. The way this would work is buying the $14 call and selling the $16 call, both expiring in two to four weeks. That gives defined exposure to a squeeze into the $15 area while keeping costs low. If the move plays out and momentum slows, one could then buy a longer-dated put, one or two months out, slightly in the money. That prepares for a retracement while taking advantage of elevated implied volatility. If the call spread hits full value early, the profit can be rotated into the put. The structure allows participation on the way up, then flips cleanly into a short with limited risk. But ultimately, if you don’t want volatility in your trading/investing life then I personally would stay away from Rigetti.

Final Thoughts

Rigetti is a difficult stock to value, but an easy one to explain. It sits in a niche, controls its own hardware, and has built real infrastructure around quantum computing. Quantum computing has been a somewhat theoretical project with little real-world application so far. The success of Rigetti is closely tied to the future of the technology. I’m personally bullish on quantum computing, and I’m certain it will change the world as we know it. Whether Rigetti is still around by the time it does, who knows?

I hope you found this article both engaging and informative. If you know someone who might find this article interesting, passing it along would mean a lot and helps grow the page. Thank you for reading and stay tuned for the next article!

Disclaimer: This article is for informational purposes only and should not be considered financial or investment advice. The views expressed are my own and based on publicly available information, market trends, and personal analysis. Readers should conduct their own research and consult a financial professional before making any investment decisions.